Buy Cyient DLM Ltd for the Target Rs. 470 by Motilal Oswal Financial Services Ltd

Muted performance amid high defense revenue base

Operating performance beats estimates

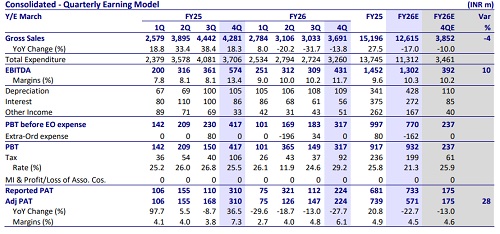

* Cyient DLM’s (CYIENTDL) 4QFY26 consolidated revenue/EBITDA declined ~14%/25% YoY to INR3.7b/INR431m, owing to a higher base of BEL orders and geopolitical disruptions in West Asia. EBITDA margins contracted 170bp YoY due to operating deleverage.

* However, the order book increased by 27% YoY/3% QoQ to INR24.2b, boosted by an order intake of ~INR4.4b. The book-to-bill ratio stood at ~1.9x in FY26. Further, the company expects FY27 to be better than FY26, led by new client additions, improving order book, and high-margin orders. These factors should help CYIENTDL to sustain 4Q-level margins in FY27.

* With a better book-to-bill ratio of 1.9x and the lower base in FY26, we believe CYIENTDL will clock a CAGR of 24%/36%/61% in revenue/EBITDA/ adj. PAT over FY26-28E. We largely maintain our earnings estimates and reiterate our BUY rating on the stock with a TP of INR470 (25x FY28E EPS).

Growing order intake improves growth outlook

* Consol. revenue declined 14% YoY to INR3.7b (est. INR3.9b), impacted by the completion of an order in Defense & Aerospace (BEL) and geopolitical uncertainties.

* The company’s order backlog expanded 27% YoY to INR24.2b, driven by a strong order intake of ~INR4.7b. Revenue from Aerospace/Industrial/ Others grew 2%/72%/72% YoY, while Defense/Med Tech declined 68%/28% YoY.

* EBITDA margins declined 170bp YoY to 11.7% (est. 10.2%). EBITDA fell 25% YoY to INR431m (est. INR392m). However, gross margin expanded 470bp to 39.1% due to an improved product mix. Adjusted PAT was down 28% YoY at INR224m (est. INR175m).

* In FY26, revenue/EBITDA/adj. PAT declined 17%/10%/23% to INR12.6b/ INR1.3b/INR571m. CFO stood at INR539m (vs. cash outflow of INR600m in FY25) and net cash was INR397m (vs. INR440m in FY25).

Highlights from the management commentary

* Outlook: Management expects YoY growth across all quarters of FY27, with a book-to-bill ratio of over 1x, while executing a phased strategy of strengthening core markets and capabilities (by FY26-27), expanding into automotive, defense and AI-led opportunities with M&A and integration (by FY27-29), and transitioning toward a product-platform-led model (by FY27-32). Margins are expected to remain stable.

* Order book: Management highlighted that order book growth will be driven by a strengthened sales team, sharper go-to-market execution, higher conversion of large deals, ramp-up in the build-to-spec (B2S) and automotive programs, new client additions, deeper wallet share with existing customers, and stable traction across diversified end-markets and geographies.

* Demand environment: The industry is expected to clock healthy growth, supported by structural drivers such as rising electronification, increasing defense spending, supply chain realignment, and AI-led demand, with welldiversified global exposure (across APAC, North America and EMEA) and a growing domestic opportunity, further reinforced by the company’s improving industry recognition.

Valuation and view

* We expect 4QFY26 to be the last quarter of earnings decline (due to high base), and anticipate growth momentum to pick up in 1QFY27. Going ahead, margins are expected to expand, driven by an improved product mix and increasing orders of box-build and B2S. Macro tailwinds, such as increasing defense spending across regions and growth in AI, are expected to drive growth in the medium term.

* For CYIENTDL, we estimate a CAGR of 24%/36%/61% in revenue/EBITDA/ adj. PAT over FY26-28. We reiterate our BUY rating on the stock with a TP of INR470 (25x FY28E EPS).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412