Buy Cello World Ltd for the Target Rs. 480 by Motilal Oswal Financial Services Ltd

Writing instrument drives overall growth

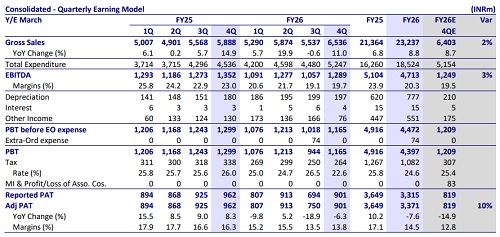

Operating performance in line with estimates

* Cello World (CELLO) reported a weak quarter, with EBITDA declining 5% YoY due to higher costs associated with the new glassware plant and steel bottle manufacturing unit, along with slow consumer demand across categories.

* While consolidated revenue grew 11% YoY to INR6.5b, growth was primarily driven by the writing instruments segment (up 64% YoY) and the consumerware segment (up 7% YoY). Growth was partially offset by a decline in the molded furniture and allied products segment (down 14% YoY).

* Ongoing supply chain issues amid the West Asia crisis and weaker demand environment are expected to impact growth in the near term. Moreover, the company expects a 10-12% revenue growth in FY27, with pickup expected gradually due to increasing utilization in the glassware plant, scaling of the steelware, and growth in the writing instruments segment (through Cello and Unomax).

* Factoring in the weak macro environment, subdued demand, and management guidance, we cut our FY27E/FY28E earnings by 9%/6%. We reiterate our BUY rating with a TP of INR480 (premised on 23x FY28E EPS).

Margin under pressure due to higher RM prices and operating deleverage

* In 4QFY26, CELLO's consol. revenue grew 11%/18% YoY/QoQ to INR6.5b (est. INR6.4b), largely led by the writing instruments business (up 64% YoY), which was supported by strong traction in newly launched products, particularly within the premium pen category.

* EBITDA declined ~5%, while it grew 22% QoQ to INR1.3b (est. INR1.3b). EBITDA margin contracted 320bp YoY and expanded sequentially 60bp QoQ to 19.7%. Adj. PAT declined ~6%, while growing 20% QoQ to INR901m (est.INR819m).

* Consumerware segment’s revenue (66% of total revenue in 4QFY26) grew 7% YoY, while it grew 13% QoQ to INR4.3b, led by steady performance in glassware and opalware. Gross margin contracted 560bp YoY due to glassware growing without profits, a 5-6% contraction in steelware margins owing to higher OEM buying costs, and a product mix shift toward lowermargin appliances.

* Further, molded furniture and allied products (~14% of the revenue mix) declined 14% YoY to INR915m due to subdued demand conditions.

* For FY26, revenue increased ~9% YoY to INR23.2b, while EBITDA/Adj. PAT declined ~8%/8% YoY to INR4.7b/INR3.4b. Cash flow from operations stood at INR2.6b as of Mar’26 (vs INR2.6b in Mar’25). Net cash position for FY26 stood at INR7b (vs INR6.6b YoY).

Highlights from the management commentary

* Steel bottle production: The steel products facility did not contribute materially in 4QFY26. Operations commenced in 4QFY26 with two production lines, followed by commissioning of an additional four lines in 1QFY27 and two more lines planned for 2QFY27. With all phases expected to be installed by Jul’26, the company anticipates full-scale production thereafter. The facility has a peak revenue potential of ~INR3b.

* Writing Instruments (WI): The company is expanding its presence in the INR12/15 pen category, thereby reducing dependence on the INR10 segment. Further, expansion into markers, sketch pens, and crayons is expected to drive a scale-up in the segment. The company is targeting revenue of at least INR5b from this segment in FY27.

* Glassware: The glassware facility is currently operating at ~60% utilization and is being adversely affected due to Chinese dumping. However, the long-term potential remains promising due to the changing product mix and better quality than Chinese imports. Increasing utilization and rising dollar are expected to improve profitability of this segment.

* Guidance and outlook: Management has guided for revenue growth of ~10-12% in FY27 despite prevailing geopolitical challenges. EBITDA margins are expected to expand by ~200-250bp (vs FY26 margins of 20.3%), supported by the ramp-up of the steel facility and recovery in glassware profitability. The company is preserving cash as it is evaluating inorganic opportunities.

Valuation and view

* While FY26 was marked by multiple headwinds and evolving market conditions across industries , with some key products witnessed near-term challenges. Management remains focused on: 1) enhancing operational efficiency, 2) rationalization of its product portfolio, and 3) realignment of its distribution strategy.

* The writing instruments segment is expected to continue its strong momentum, supported by the addition of the Cello brand to its portfolio and the expansion into other stationery items. Meanwhile, the consumerware segment is expected to stabilize from 2HFY27 onward, driven by the ramp up of its steel bottle manufacturing capacity, improved capacity utilization in the glassware segment, and the launch of new products.

* We expect CELLO to register a 12%/20%/18% revenue/EBITDA/Adj. PAT CAGR over FY26-28. We reiterate our BUY rating with a TP of INR480 (premised on 23x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)