Buy Awfis Space Solutions Ltd For Target Rs. 760 By Choice Broking Ltd

Profitable Growth Ahead

Relying on its Proven Business Model!

We continue to maintain our BUY rating with a marginally higher TP of INR 760/sh (750 /sh earlier) on AWFIS. Despite factoring in seat addition growth slower than previous years (FY25 – 28E CAGR of 14% vs FY22 – FY25 of 43%), we forecast EBITDA CAGR of 21% over the period. In the organised sector, there is a long list of competitors such as, WeWork India, Smartworks, Indiqube, Tablespace, EFC(I), Redbricks and BHIVE. Players in the unorganised segment which could also compete aggressively with AWFIS. However structural growth in the managed office space sector and AWFIS’s established presence over the years as a reliable and premium provider are sufficient reasons for the company’s prowess to maintain its market share. We expect contribution margin to increase marginally owing to operating leverage benefit, premiumisation, value-added services, etc.

Valuation: We incorporate an EV/Adjusted EBITDA framework where the adjusted EBITDA is IGAAP-based. We value the stock at 1-year forward EV/Adjusted EBITDA multiple of 16x, which translates into a target price of INR 760 per share, implying an upside of 20%, with a BUY rating on the stock.

Valuation: We incorporate an EV/Adjusted EBITDA framework where the adjusted EBITDA is IGAAP-based. We value the stock at 1-year forward EV/Adjusted EBITDA multiple of 16x, which translates into a target price of INR 760 per share, implying an upside of 20%, with a BUY rating on the stock.

Risks: Possible slowing down of demand from GCC and startups, probable decrease in blended occupancy levels and intensified competition from peers.

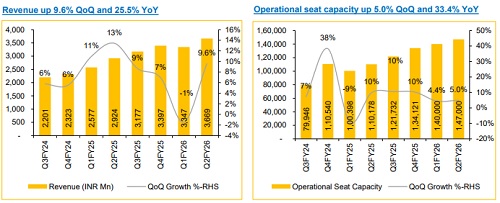

Q2FY26 Review: Healthy revenue growth and seat addition

* Revenue for Q2FY26 was reported at INR 3,669Mn, up 25.5% YoY and down 9.6% QoQ vs CIE estimate at INR 3,980Mn.

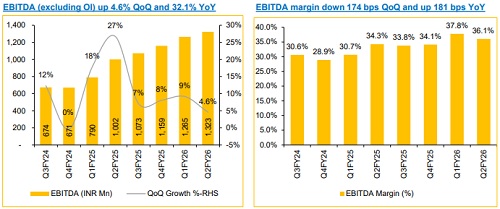

* EBITDA (excluding OI) for Q2FY26 was reported at INR 1,323Mn, up 32.1% YoY and 4.6% QoQ vs CIE estimate at INR 1,382Mn.

* IGAAP-adjusted EBITDA for Q2FY26 was INR 520Mn, up 18.2% YoY and 8.3% QoQ. IGAAP-adjusted EBITDA margin came in at 14.1% vs 14.9% in Q2FY25 and 14.5% in Q1FY26.

* In Q2FY26, total seats (operational + fitout) stood at 1,70,000 vs 1,55,490 in Q1FY26 and total operational seats increased 5.0% QoQ and 33.4% YoY.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)