Buy 360 One Wam Ltd for the Target Rs. 1,300 by Motilal Oswal Financial Services Ltd

Operating performance in line

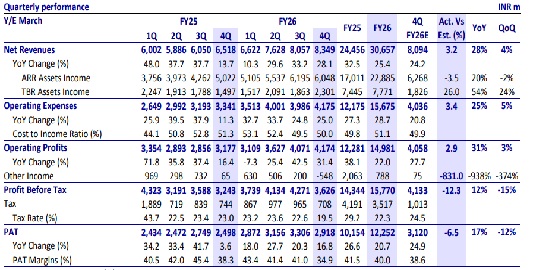

* 360 One WAM (360ONE) reported a 4QFY26 operating revenue of INR8.3b (in line). Its operating revenue grew 28% YoY, driven by 20% YoY growth in recurring revenue and 54% YoY growth in transactional revenue. For FY26, the company’s operating revenue grew 25% YoY.

* The cost-to-income ratio at 50.1% declined 120bp YoY (MOFSLe – 49.9%), with operating profit at INR4.2b (in line), which grew 31% YoY. For FY26, its operating profit came in at INR15b, up 22% YoY.

* Negative other income of INR550m resulted in a 6% miss on PAT. Its PAT rose 17% YoY to INR2.9b. For FY26, the PAT grew 21% YoY to INR12.2b.

* Management expects net flows of ~12–15% of opening AUM annually, supported by brand strength and talent expansion, along with MTM gains of ~10–12%. The cost-to-income ratio of ~49-50% is likely to moderate to ~46-48% through efficiencies in core and scaling of new businesses.

* We slightly cut our EPS by 1%/3% for FY27E/28E, considering an increase in costs owing to RM hiring as well as IB team build-up. We adopt the SoTP approach, valuing ARR at 36x FY28E PAT and TBR/other income at 20x FY28E PAT, to arrive at a fair value of INR1,300. Reiterate BUY.

Organic flows broadly stable; MTM impact on AUM

* 360ONE reported net ARR inflows of INR90b in 4QFY26 compared to INR40b in 4QFY25. On the wealth management side, ARR net flows stood at INR69.6b (INR33.2b in 4QFY25). AMC net flows were at INR20.3b compared to INR6.7b in 4QFY25.

* Wealth management ARR’s AUM grew 33% YoY to ~INR2.2t, driven by 37%/31%/37% YoY growth in 360 One Plus/Distribution/Lending AUM. Robust inflows were observed in 360 ONE Plus and the lending book, while distribution assets experienced outflows (mainly in the treasury book).

* Wealth management ARR’s retention stood at 74bp (vs. 80bp in 4QFY25), with the YoY dip largely led by a decline in lending book retention to ~5.25% (from 5.7% in 4QFY25). In contrast, the distribution and 360 ONE Plus retention were largely stable.

* Asset management AUM grew 13% YoY to INR952b, driven by 26%/9% YoY growth in AIF/MF AUM while discretionary PMS declined 4% YoY. The segment added ARR net flows worth INR20.3b with some redemptions seen in credit, private equity, and real estate funds.

* Asset management yields stood at 86bp (90bp in 4QFY25), with DPMS retention reducing and AIF retention rising YoY. Strategic recalibration is ongoing to improve the performance in DPMS.

* Employee costs grew 19% YoY to INR3b (in line) and the company aims to continue adding RMs as well as senior managers. Other admin costs grew 45% YoY to INR1.2b (in-line), resulting in total costs of INR4.2b.

* Other income was negative at INR548m in 4QFY26 (vs. INR65m in 4QFY25)

Highlights from the management commentary

* Attrition remains a risk, though mitigated by a diversified workforce, with ~60– 65% of employees having 8–9 years of tenure. Management is comfortable with ~2–4% annual attrition.

* Carry accounting remains conservative, with carry AUM at ~75–80% of ARR AUM. Carry accruals are ~5–7bp in weak years and ~12–15bp in strong years, subject to meeting fund-level hurdles over the entire lifecycle.

* Transactional brokerage in 4Q reflects full-quarter consolidation of B&K. Fixed income, REITs, and InvITs supported growth. The quarterly TBR is expected to stabilize at INR1.6-1.8b (vs. INR1.2-1.4b earlier).

Valuation and view

* 360ONE offers a compelling structural growth story anchored to India's expanding wealth and asset management market. The company continues to garner robust flows across wealth and asset management, which are likely to be supported by the onboarding of new teams. The acquisition of B&K and the UBS collaboration enhance the company’s international footprint, broaden client access, and strengthen its transactional platform. Operating leverage and cost synergies from integrations are anticipated to improve the company’s profitability as new businesses scale up.

* We have slightly cut our EPS estimates by 1%/3% for FY27/28, considering an increase in costs owing to RM hiring as well as IB team build-up. We adopt the SoTP approach, valuing ARR at 36x FY28E PAT and TBR/other income at 20x FY28E PAT, to arrive at a fair value of INR1,300. Reiterate BUY.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412