Bulls and Bears : Weakness continues; India lags global peers by Motilal Oswal Financial Services Ltd

Weakness continues; India lags global peers

* Tested by volatility, the Nifty consolidates in May’26: The Nifty consolidated (down 1.9% MoM) in May’26 after rebounding smartly in Apr’26 with a 7.5% MoM gain. Notably, the index remained volatile and hovered around 1,220 points before closing 450 points lower. The Nifty is down 9.9% in CY26YTD. Over the last 12 months, largecaps have been down 5%, underperforming midcaps and smallcaps, which have been up 7% and 1%, respectively. Over the last five years, midcaps (CAGR: 19.1%) have notably outperformed largecaps (CAGR: 8.6%) by 88%, while smallcaps (CAGR: 14.4%) have markedly outperformed largecaps by 45%.

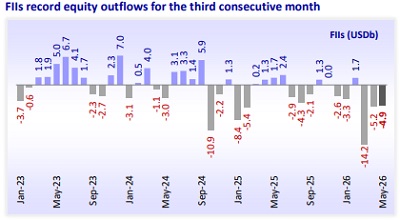

* FIIs record outflows for the third consecutive month; DII inflows remain strong: FIIs recorded outflows for the third consecutive month in May’26 at USD4.9b. Notably, DII inflows were strong at USD8.7b. FII outflows into Indian equities stand at USD25.9b in CY26YTD. DII inflows into equities continue to be strong at USD41.4b in CY26YTD.

* Breath balanced in May’26: Sector wise, Telecom (+16%), Metals (+5%), Capital Goods (+5%), Healthcare (+5%), and Power (+3%) were the top gainers MoM, while PSU Banks (-4%), Consumer (-3%), Media (-3%), Real Estate (-1%), and Technology (-1%) were the key laggards. The breadth was balanced in May’26, with 24 Nifty stocks closing higher. Adani Enterprises (+22%), Tata Motors PV (+15%), Grasim (+12%), Asian Paints (+9%), and Adani Ports (+9%) were the top gainers, while ONGC (-11%), SBI (-10%), ITC (-9%), Power Grid (-9%), and TCS (-9%) were the key laggards.

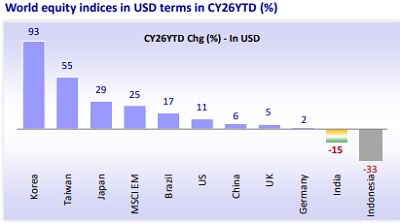

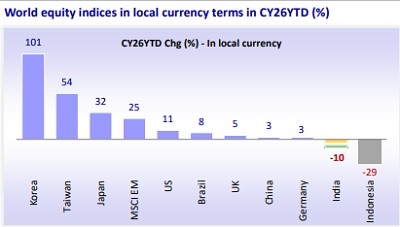

* Major economies end higher in May’26: Among the key global markets, Korea (+28%), Taiwan (+15%), Japan (+12%), MSCI EM (+9%), the US (+5%), Germany (+3%), and the UK (+0%) ended higher MoM. However, Indonesia (-12%), Brazil (-7%), India (-2%), and China (-1%) ended lower MoM. During the past 12 months, the MSCI India Index (-11%) has underperformed the MSCI EM Index (+51%) in USD terms. Over the last 10 years, the MSCI EM Index has now outperformed the MSCI India Index by 12%.

* Earnings review 4QFY26: The 4QFY26 corporate earnings concluded on a strong note, showcasing widespread outperformance across aggregates. BFSI, Metals, OMCs, Technology, Telecom, and Automobiles fueled this healthy performance. Conversely, Oil & Gas (ex-OMCs) dragged overall profitability. The aggregate earnings of the MOFSL Universe companies grew 16% YoY (vs. our est. of 8% YoY) in 4QFY26. The Nifty delivered a 4% YoY PAT growth (vs. our est. of +2%). Nifty reported a single-digit earnings growth for the eighth consecutive quarter since the pandemic (Jun’20). Barring Reliance Industries, which posted a profit dip of 13% YoY, and Interglobe Aviation, which posted a loss of INR24b vs. a profit of INR30.7b YoY, the Nifty Universe posted a 9% YoY earnings growth.

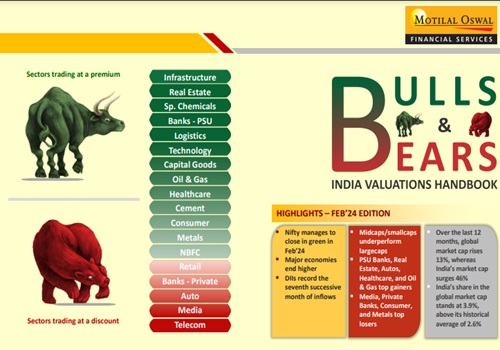

* The Nifty-50’s valuation below its historical average: The Nifty is trading at a 12-month forward P/E ratio of 18.6x, below its LPA of 21x (at an 11% discount). Further, its P/B of 2.7x represents a 5% discount to its historical average of 2.9x. The 12-month trailing P/E for the Nifty, at 21.5x, is below its LPA of 23.2x (at a 7% discount). At 3x, the 12-month trailing P/B ratio for the Nifty is below its historical average of 3.2x (at a 4% discount). Notably, twothirds of the sectors trade at a discount to their averages. Capital Goods, PSU Banks, Metals, Oil & Gas, Healthcare, and Utilities trade at a premium to their long-period average (LPA) valuations, while Private Banks, Consumer, Technology, and Retail trade at a discount to their LPA.

* View: The Nifty-50 registered a modest 5% EPS growth in FY26 (following a 16%+ CAGR during FY20-25). Following India’s sharp underperformance in FY26 and record FII outflows, a favorable base has likely been set for Indian equities. However, in the near term, the market will remain hostage to volatile developments arising from the West Asian crisis. Higher commodity prices will be the key monitorables, as a prolonged elevated level could affect India’s macro parameters and engender a tight monetary policy stance. Our model portfolio broadly reflects our preference for growth visibility, structural domestic growth plays, and select global value names. We firmly believe that this is a bottom-up market, despite India witnessing both time and price corrections relative to EM peers. Our key OW sectors are Autos, PSU Banks, Diversified Financials, Manufacturing & Industrials, Consumer Discretionary, and New-age platforms. In contrast, we are UW on Oil & Gas, Private Banks, Metals, Consumer Staples, IT, and Commodities/Utilities.

* Top Nifty-50 Ideas: Bharti Airtel, SBI, ICICI Bank, M&M, Titan, Bharat Electronics, Eternal, Tata Steel, Infosys, and Interglobe Aviation. Top Non-Nifty-50 Ideas: TVS Motors, ICICI PRU AMC, Groww, Indian Hotels, AU Small Finance, Dixon Tech., Lenskart, Waaree Energies, Coforge, Radico Khaitan, and Delhivery

FIIs record outflows for the third straight month; DII inflows remain strong

India underperforms key global markets in CY26YTD

* The Nifty consolidated (down 1.9% MoM) in May’26 after rebounding smartly in Apr’26 with a 7.5% MoM gain. Notably, the index remained volatile and hovered around 1,220 points before closing 450 points lower. The Nifty is down 9.9% in CY26YTD.

* Sector wise, Telecom (+16%), Metals (+5%), Capital Goods (+5%), Healthcare (+5%), and Power (+3%) were the top gainers MoM, while PSU Banks (-4%), Consumer (-3%), Media (-3%), Real Estate (-1%), and Technology (-1%) were the key laggards.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412