AI Strategy Sector Update :AI's Glass House: Faultlines Threatening the Rally by Elara Capital

The recent global sovereign bond sell-off, driven by renewed inflation risks from energy shocks and disrupted supply chains, has clouded the outlook of asset markets. US yields remain elevated, roughly 50bp above pre-war levels (two-year up ~60bp as on end-May 2026), even as AI rallies on new product launches, booming demand for high-bandwidth memory and infrastructure hardwares. We identify key fault lines in the AI expansion — escalating input cost, heavier debt-funded capex in a scenario of rising interest rate, and growing energy imbalances — that could interrupt the market’s presumed one-way upward move.

History shows surge in yield precedes equity bubble bursts:

During every crisis and bubble burst episode since the 1990s, the benchmark US 10y yield on average rose 92bp from its TTM bottom before peaking. As on 1 June 2026, the yield rose 50bp from its TTM bottom with the potential to rise further if inflationary pressures in US become entrenched dislodging inflation expectations forcing Fed to toughen its stance on inflation, and lingering fiscal risks amplify as election and budgets come closer. This has the potential to pose potent challenges for current equity rally, which is led by AI and AI+ stocks.

Rising yield can disrupt the AI rally as cost of capital rises:

Latest volatility in the private credit market can amplify if short term rates move up if Fed points to rate hikes as SOFR acts as benchmark for private credit markets. As per the BIS, lending by private credit funds to AI-related sectors has grown rapidly, both in absolute terms and as a share of total private credit volume. Outstanding loan amounts have increased from near-zero to >USD 200bn as on CY25. The share of private credit loans to AI-related companies has increased from less than 1% of total outstanding loan volume to ~8%.

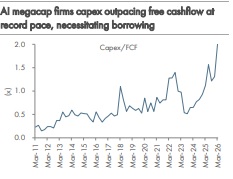

AI-driven corporate issuance is emerging as a meaningful source of duration supply in US fixed income. According to the Federal Reserve of Dallas, AI-related investment-grade issuance amounted to ~USD 190bn in CY25, 3.4x of CY24. As per S&P Global, data center debt issuance nearly doubled to USD 182bn in CY25 vs CY24. Our analysis shows capex by mega tech firms, including hyperscalers, has surpassed free cashflow, with capex/FCF ratio above 1x (the highest since CY95), indicating further borrowing needs on the pipeline.

Input price surge and accelerated hardware obsolescence mean additional funding needs:

Higher power prices and input inflation is compressing margin with several projects needing stronger utilization and faster revenue ramp-up to hit target ROI. The IMF's January 2026 WEO warned that "frequent equipment upgrades (GPU refresh cycles) will squeeze profit margin requiring significant additional debt financing". If the hyperscalers, (at USD 700bn capex), were to reflect realistic obsolescence of hardware at three years instead of five, then depreciation cost would rise by USD 93bn, leading to additional debt financing. The second fault line runs through the semiconductor and memory supply chain. Memory prices have risen ~50% YTD through late CY25, with Trendforce projections pointing to a further doubling through CY26. Stripping out memory price inflation, and hyperscaler capex growth decelerates from ~80% in CY25 to ~40% in CY26.

Energy is the most immediate physical constraint on AI expansion:

Data center electricity consumption in US surged 17% in CY25, and the US Department of Energy estimates data centres could account for 6.7–12.0% of total US electricity consumption by CY28, up from ~4% in CY23. While the US has the investment intent to expand grid capacity, the mix is incorrect - too intermittent, year-long queues, with baseload firm power -- natural gas and nuclear are not expanding rapidly to match pace of data center demand. The EIA Annual Energy Outlook 2026 projects nuclear capacity to remain flat through the 2030s — despite nuclear being the only large-scale, firm, zero-carbon source capable of anchoring AI data center loads. The 241GW data centre project pipeline in the US is chasing ~86GW of annual new utility-scale electric generating capacity, defining grid tension of the AI buildout

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...