No Record Found

Latest News

Equirus sole advisor to Kalpataru Projects on Vindhy...

Quote on Tech (AI) Budget Expectation by Akshay Chha...

Quote on Pre Budget by Mr. Sudarshan Lodha, Co-found...

Trade pacts with developed economies to boost startu...

Expectations on Union Budget 2026?27 by Dilip Modi, ...

Expectations on Union Budget 2026?27 by Mat?as Gainz...

Bank of India, Mumbai North Zone Hosts ``Pravasi Sam...

Kotak Mutual Fund Launches Kotak Nifty200 Value 30 I...

Kishan Reddy urges CM Revanth Reddy to expedite take...

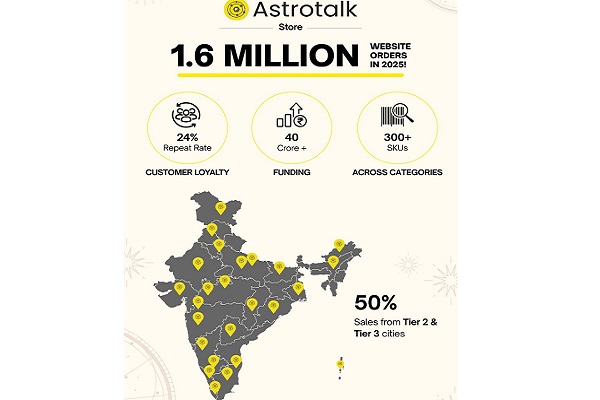

Astrotalk Store - From a Rs 30 lakh investment to Rs...

Top News

News Not Found

Tag News

News Not Found

More News

News Not Found